RBI Cuts Repo Rate, Raises GDP Outlook: Big Announcements from the Final Policy Meet of 2025

The Reserve Bank of India has intensified its efforts to improve customer service across the financial sector, highlighting initiatives such as simplified Re-KYC norms, digital service access, and nationwide financial awareness programmes. The central bank noted that over 99.8% of service-related applications are now being disposed of within the prescribed timeline. However, a rise in consumer grievances has increased the pendency burden with the RBI Ombudsman. To address this, the RBI will launch a two-month special campaign from January 1 to clear all complaints pending for more than 30 days, urging all regulated entities to prioritise customer-centric operations.

During the Monetary Policy Meeting, RBI Governor Sanjay Malhotra confirmed that India’s forex reserves stand at USD 686 billion, offering over 11 months of import cover. The central bank revised GDP growth projections upward to 7.3% and highlighted strong momentum across manufacturing, services, banking credit, and rural demand. Retail inflation continues to moderate, with CPI now projected at 2% for the year. The MPC unanimously cut the repo rate by 25 bps to 5.25% while maintaining a neutral stance, reaffirming confidence in India’s stable macroeconomic outlook

Similar News

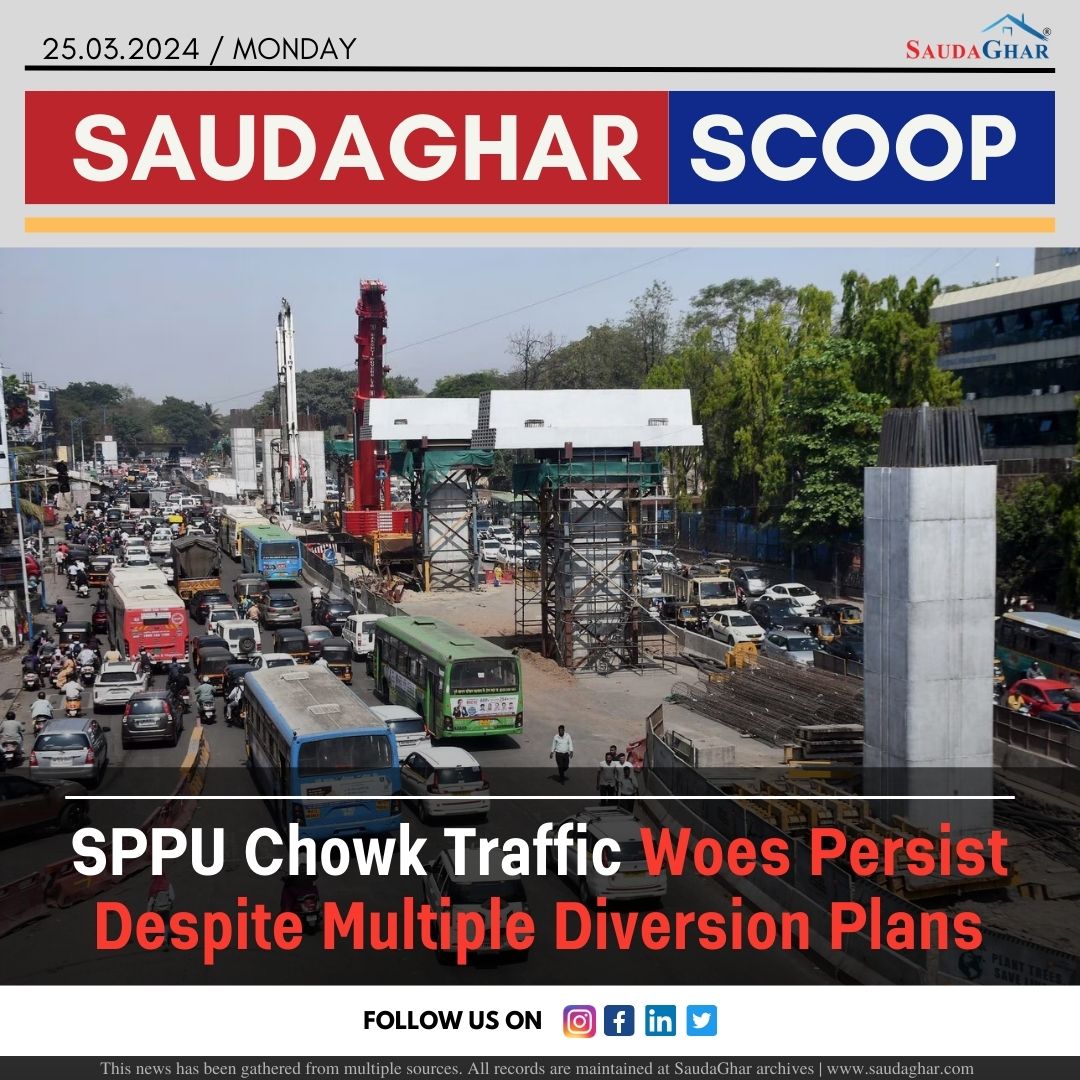

Monsoon Deluge Exposes PMC Road Repair Failures

28 Sep 2023

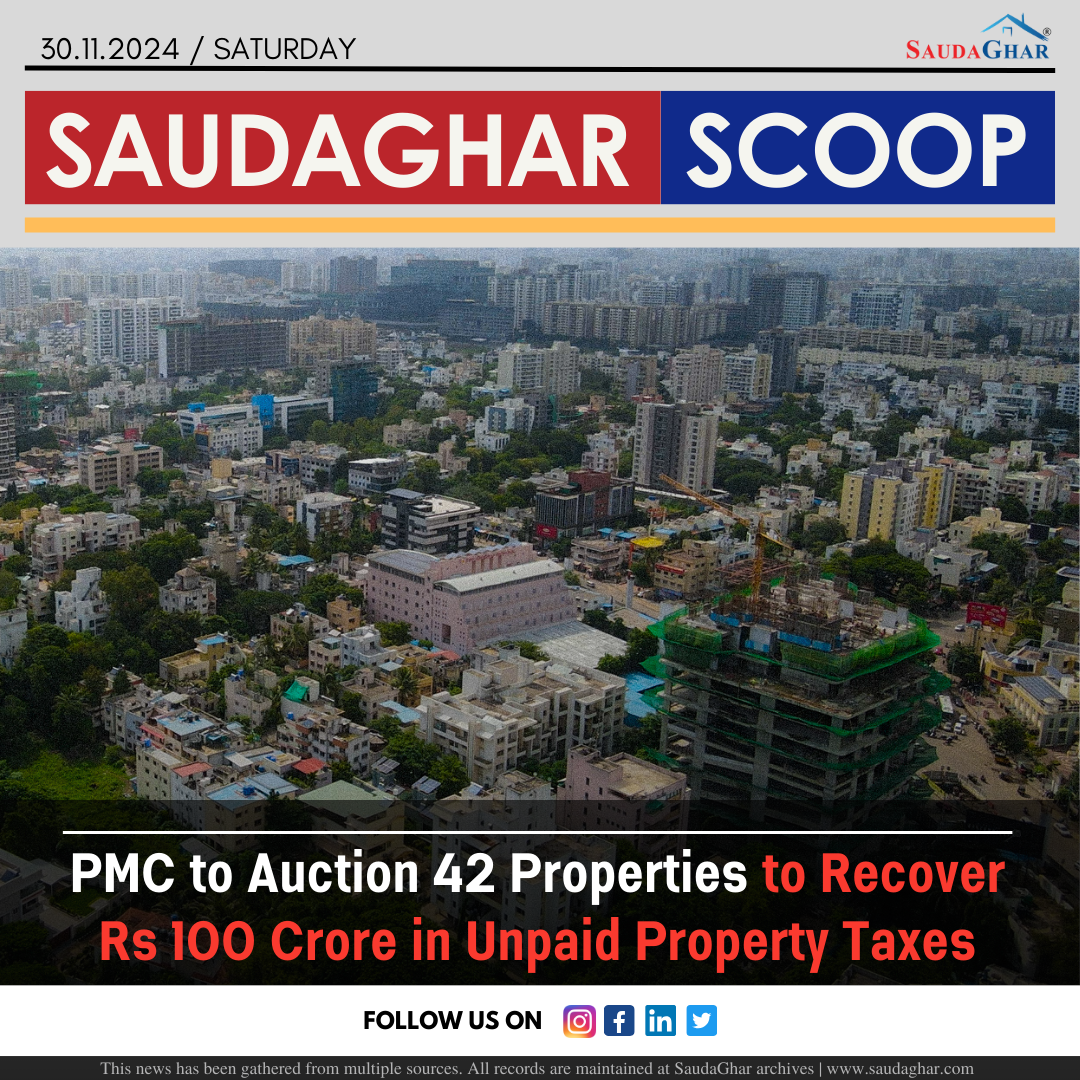

Amnesty Scheme to Reduce Stamp Duty Deficit

02 Dec 2023

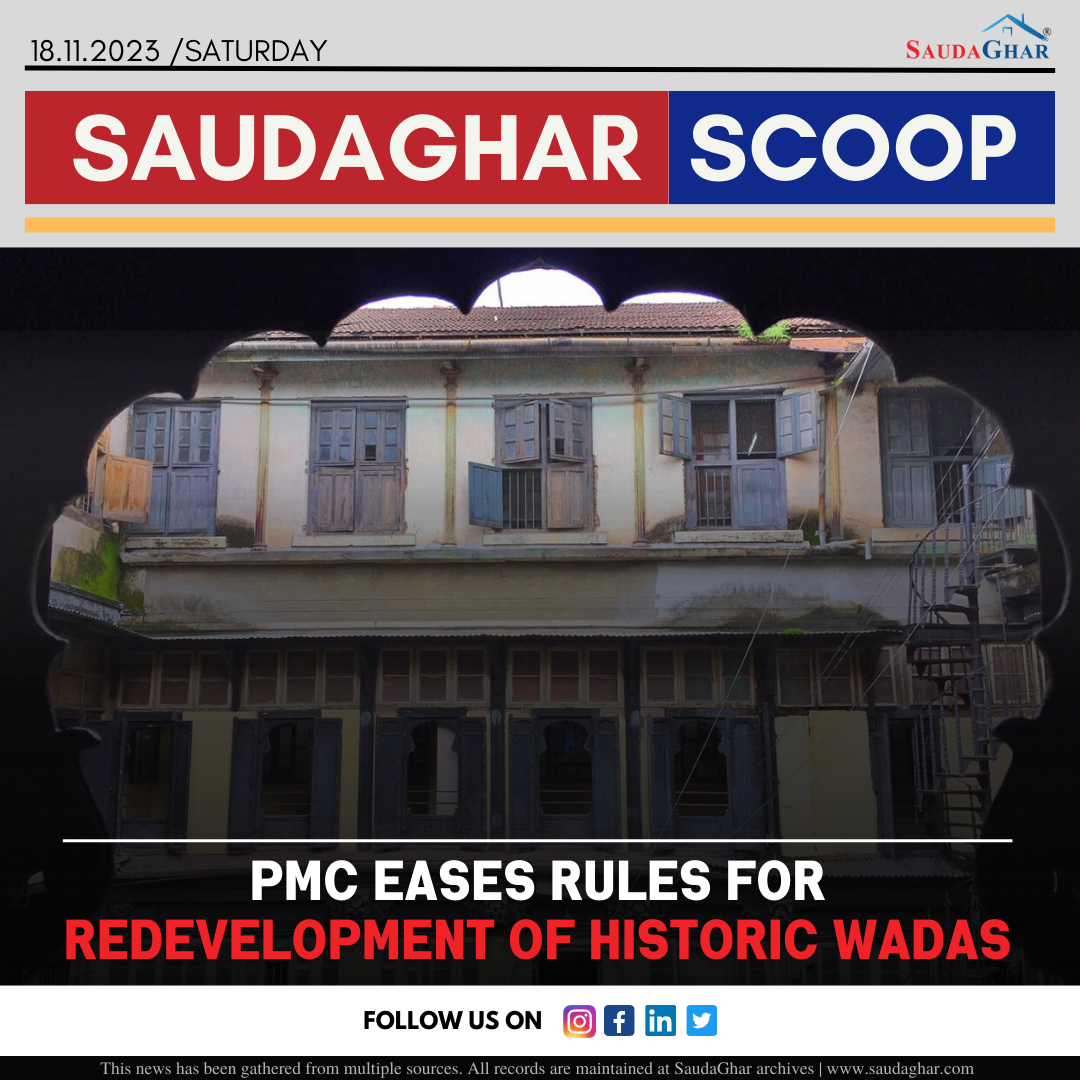

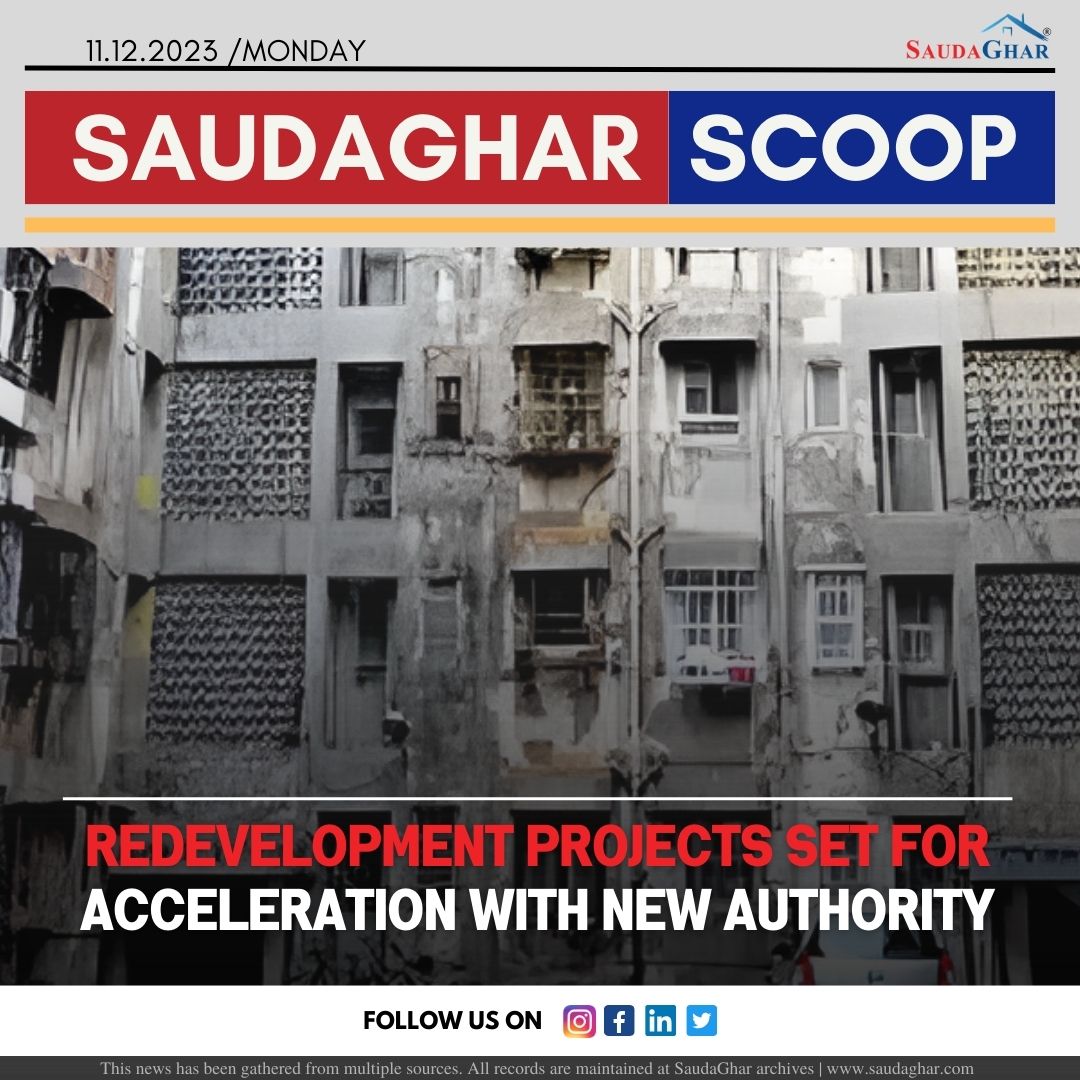

Historic Bhide Wada Set for Redevelopment by PMC

06 Dec 2023

PMC Approved Bus Bay on Nagar Road

12 Dec 2023

PMC Phased Approach to Repair 40 Aging Bridges

08 Jan 2024

Long Weekend से Pune-Satara Highway पर लगा लंबा!

27 Jan 2024

आखिर कब Open होगा Pune Airport का New Terminal?

06 Feb 2024

Pune Areas to Experience Water Shortage Tomorrow

07 Feb 2024

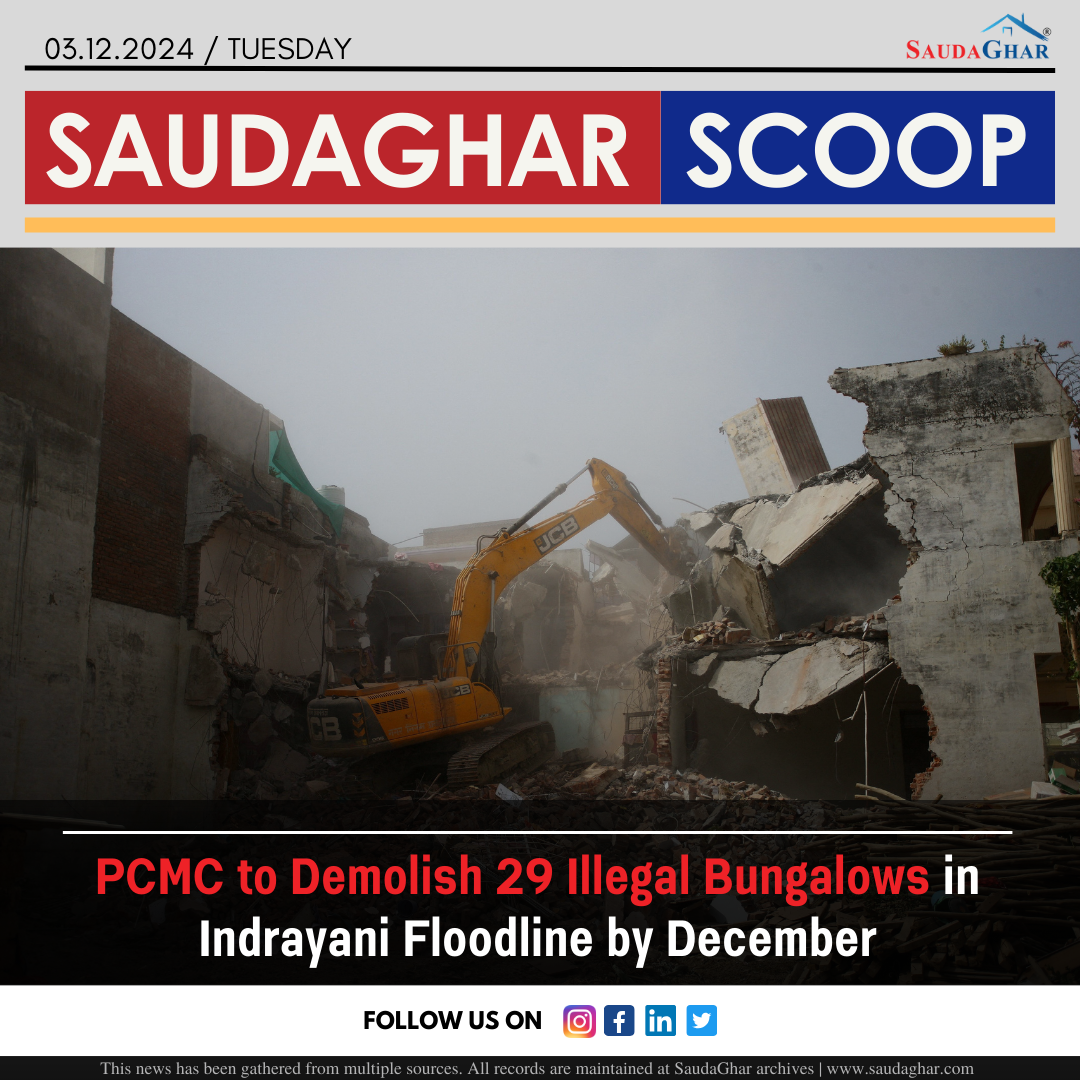

PMC demolishes 29 Hilltop Properties

09 Feb 2024

PMC under scrutiny for repeated budget inflation

03 Apr 2024

Pune Battle Against Rising Garbage-Related Fires

08 Apr 2024

IMD Warns Dry Conditions Challenge 125 Districts

19 Apr 2024

Residents Sweat Through Frequent Power Outages

28 Apr 2024

BSI to Open New Botanical Garden in Mundhwa

27 Aug 2024

KCB 326-Acre Merger with PMC Awaits Approval

25 Dec 2024

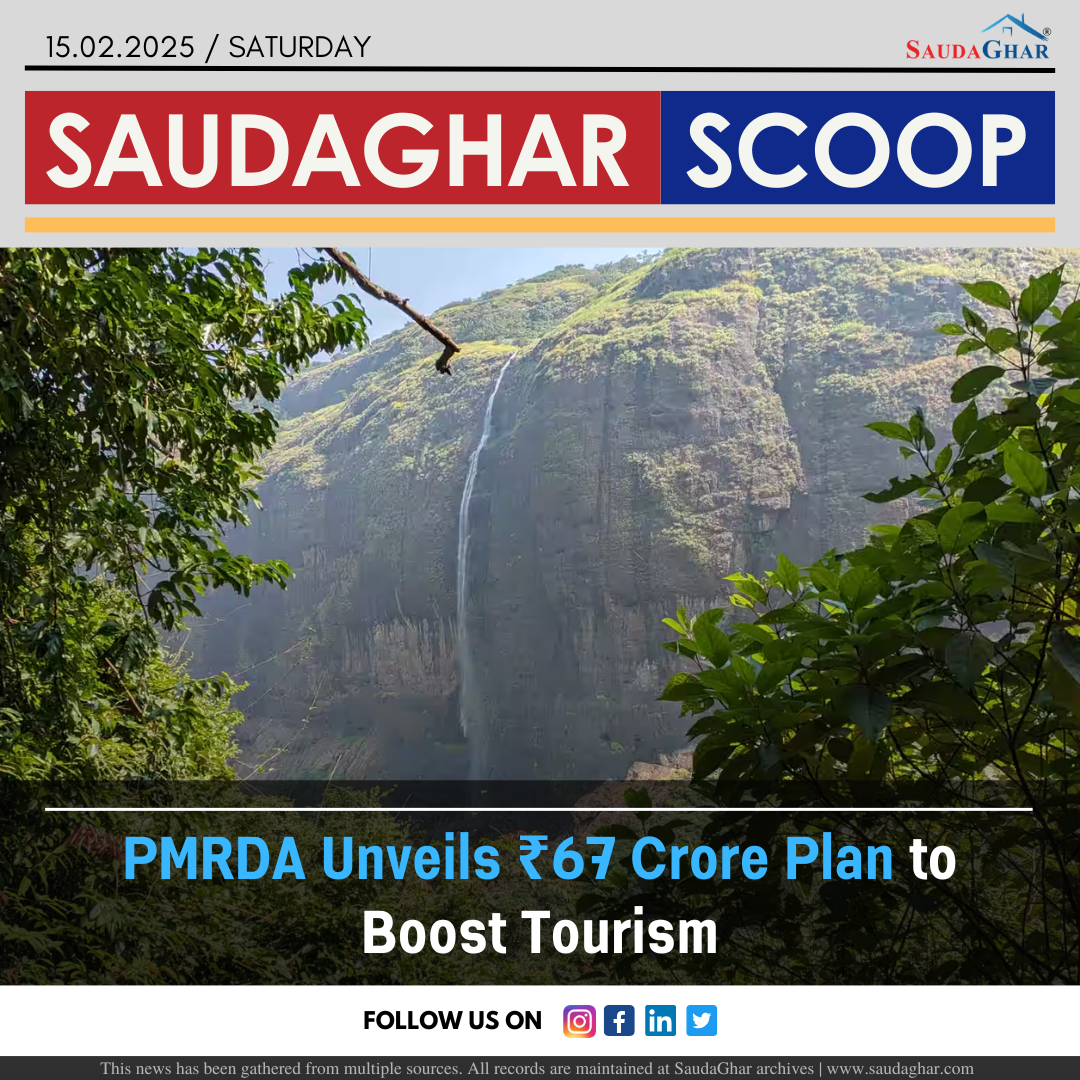

PMRDA Unveils ₹67 Crore Plan to Boost Tourism

15 Feb 2025

Land Acquisition for PMRDA Ring Road Speeds Up

20 Jul 2025

Civic Apathy Delays Pune Warje Road Project

08 Aug 2025

Why PCMC Shut Down Multiple RMC Plants.

17 Nov 2025

New Repairs Same Old Pothole Problems in Pune.

18 Nov 2025

Yerawada Katraj Tunnel A New Way to Cross Pune

07 Jan 2026

What 2025 Tells Us About Pune Real Estate Demand

09 Jan 2026